IJM Corporation Bhd, one of Malaysia’s largest construction and infrastructure groups, has come under renewed scrutiny following the resurfacing online of a whistleblower complaint that alleges the existence of opaque offshore structures, questionable shareholding arrangements and links to individuals accused of large, unreported cross-border financial transfers and income patterns inconsistent with declared tax payments in Malaysia.

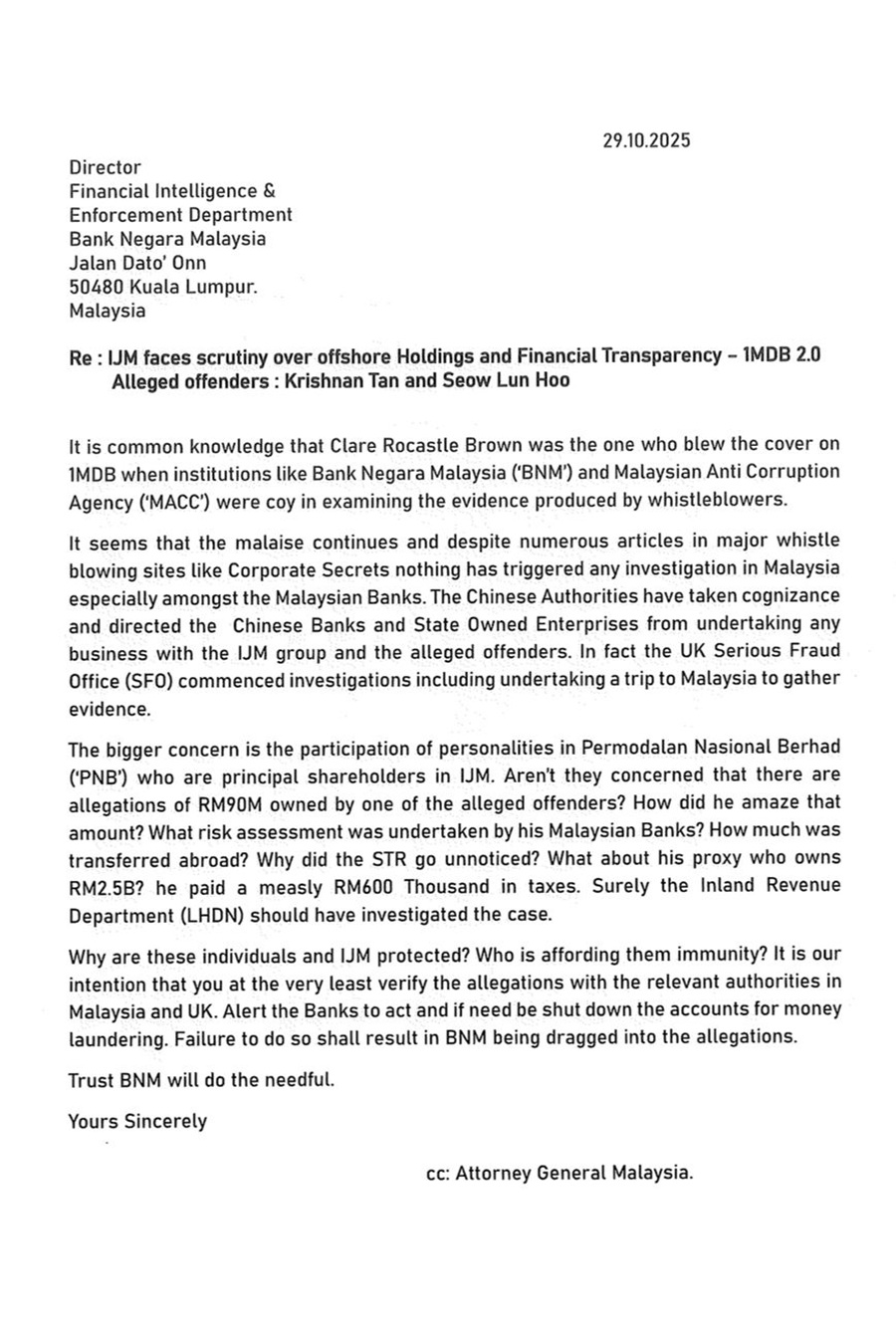

The letter, addressed to Bank Negara Malaysia (BNM) and copied to the Attorney General’s Chambers, raises a series of allegations involving two individuals identified as Krishnan Tan and Seow Lun Hoo. It also questions the adequacy of governance oversight at Permodalan Nasional Berhad (PNB), a major institutional shareholder in IJM.

Local Regulators Vs Foreign Enforcement Agencies

According to the complaint, concerns surrounding IJM and the named individuals had previously been highlighted by a Malaysian whistleblower platform but failed to trigger sustained action by local authorities or domestic financial institutions. This was despite records from the Inland Revenue Board (LHDN) allegedly indicating unusual income patterns and financial activity linked to Krishnan Tan and Seow Lun Hoo. Sources claim that IJM subsequently initiated legal action against the portal that published the exposé.

The whistleblower further alleges that Chinese authorities have taken note of the irregularities. State-owned enterprises and banks in China were reportedly instructed to refrain from conducting business with IJM and the individuals named, a move that could potentially affect IJM’s operations in the Chinese market. Such measures, according to a source familiar with the matter, are aimed at shielding China’s financial system from exposure to entities associated with suspected money laundering risks. The directives were not publicly announced, consistent with Beijing’s administrative practices.

Separately, the United Kingdom’s Serious Fraud Office (SFO) is alleged to have initiated inquiries, including dispatching officers to Malaysia to gather information. Documents reviewed reportedly indicate cooperation between Malaysian enforcement agencies and the SFO, raising questions about why foreign authorities appear to be moving faster than domestic institutions. Meanwhile, BNM, the Malaysian Anti-Corruption Commission (MACC) and the Inland Revenue Board are described as taking a “wait-and-see” approach.

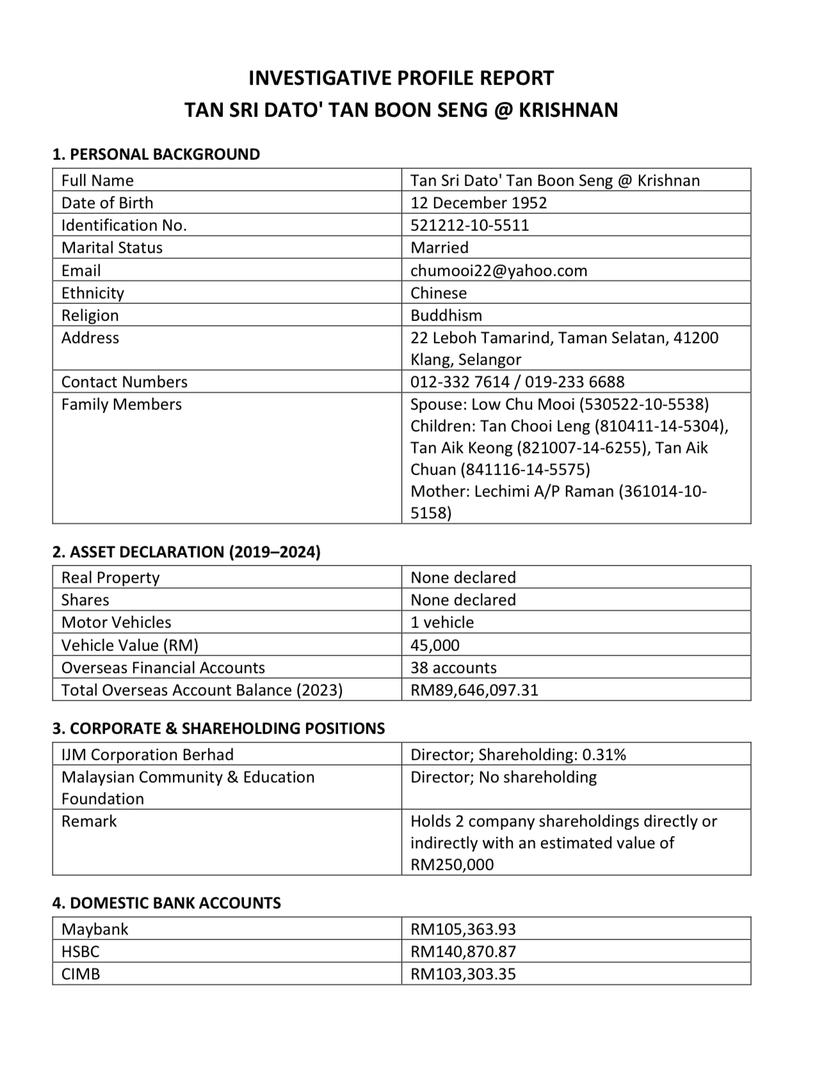

Krishnan Tan: £15.3 Million Offshore, Minimal Tax Paid

Central to the allegations is the claim that IJM chairman Krishnan Tan holds offshore accounts totalling £15.3 million (approximately RM90 million), alongside dozens of large cash and transfer transactions that remain unexplained.

A detailed review of available financial records suggests that the total volume of questionable fund flows linked to Krishnan Tan may exceed RM300 million. The whistleblower alleges that no satisfactory explanation has been provided regarding the origin of this wealth.

Official documentation reportedly records four Suspicious Transaction Reports (STRs) involving transaction patterns inconsistent with his corporate profile. In addition, 58 Cash Transaction Reports (CTRs) with a cumulative value exceeding RM183 million raise concerns over extensive use of cash, a method often associated with efforts to obscure the origin of funds. A further 25 Transfer Reports (TRs) totalling more than RM23 million suggest potential “layering” activities — the movement of funds through multiple accounts to complicate traceability.

Collectively, the pattern is described as reaching a critical risk threshold that would typically draw the attention of financial crime watchdogs, including BNM, MACC and the police under anti-money laundering frameworks. The allegations also open questions about possible concealed political financing, proxy account usage and offshore fund routing.

The whistleblower questions how such transactions went undetected, why STRs failed to trigger deeper scrutiny, and how significant capital outflows bypassed oversight by BNM and Malaysian banks.

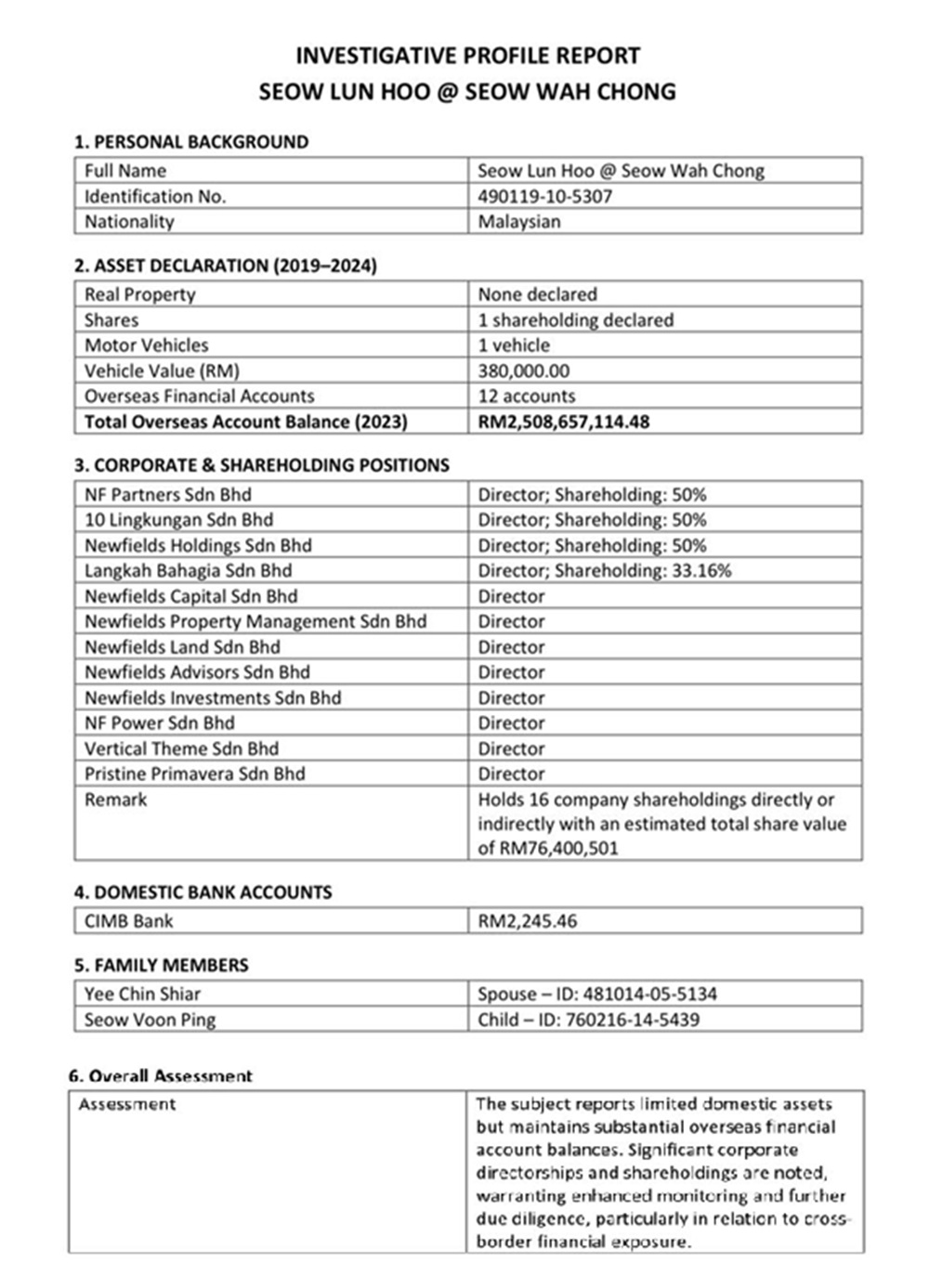

Seow Lun Hoo: RM2.5 Billion Offshore Exposure

Another individual named in the complaint, described as a close associate and proxy, is alleged to control assets worth £425 million (approximately RM2.5 billion) while paying only about £102,000 (RM600,000) in tax.

Records indicate that while only two STRs were filed in Seow Lun Hoo’s name, 68 CTRs totalling approximately RM34.5 million were recorded — an unusually high figure for a private individual. An additional 17 TRs valued at RM19.29 million point to structured fund movements between domestic and offshore accounts, potentially designed to conceal financial trails.

More striking is the existence of 12 offshore financial accounts linked to Seow, with total balances exceeding RM2.5 billion. The scale of these holdings, when viewed against his declared income, raises serious questions about the source of funds and compliance with tax and financial regulations.

Available tax records show Seow declared income of RM580,746 and paid RM102,926.46 in tax, figures that appear grossly disproportionate to the offshore assets and transaction volumes attributed to him. Observers say the disparity warrants urgent investigation by BNM, MACC, the police and foreign enforcement bodies such as the UK’s SFO.

Alleged IJM–Sunway Share Swap and Minority Shareholder Concerns

The latter part of the complaint introduces allegations of a proposed share-swap arrangement involving IJM shareholders referred to as “KT & Seow” and a high-profile individual identified as “TS Jeffrey”.

According to the complaint, the arrangement was allegedly structured at shareholder level, allowing IJM’s board to distance itself from direct involvement. TS Jeffrey is said to have been prepared to offer a premium of around 40% to acquire shares held through proxies linked to the two individuals.

The whistleblower claims such an arrangement would disadvantage minority shareholders, including PNB, potentially exposing them to losses if the transaction proceeded without transparency and adequate safeguards. The letter also references a past PNB transaction involving another major developer, which allegedly benefited a non-Malay corporate figure, raising questions about consistency in governance standards.

The complaint further speculates that, in the event of a takeover, Sunway Group — mentioned indirectly — could undertake large-scale restructuring, including the removal of IJM’s existing management and workforce. However, these claims remain speculative and unsupported by documentary evidence.

Call for Regulatory Intervention

The whistleblower urges Bank Negara Malaysia to act decisively by verifying the allegations in cooperation with Malaysian and UK authorities, alerting financial institutions, and considering enforcement measures such as freezing or closing accounts suspected of facilitating money laundering.

Failure to act, the letter argues, risks drawing Malaysian regulators into the controversy and undermining their institutional credibility. The complaint concludes by expressing confidence that BNM will act in accordance with its statutory mandate.

IJM Denies Merger Talks; Sunway Silent

In response to separate media reports suggesting a potential merger with Sunway Berhad, IJM issued a clarification to Bursa Malaysia stating that its board is not aware of any such proposal and has not been approached regarding a merger. The company reiterated its commitment to Bursa Malaysia’s disclosure requirements and said it would make announcements should any material developments arise.

Sunway Berhad, however, has yet to issue any public statement or Bursa filing to confirm or deny the speculation. Market observers note that while IJM’s clarification closes the issue from its standpoint, the absence of a response from Sunway continues to fuel uncertainty, particularly given the broader allegations involving ownership structures and minority shareholder interests.

Governance analysts stress that clear and comprehensive disclosure from all parties involved is essential to prevent prolonged speculation and to safeguard investor confidence.